Exploring second strikes, equity grant votes, board spill resolutions and serial strike recipients

In Georgeson's 2025 AGM Review we highlight some of the key high-level data on proxy voting outcomes on remuneration report and equity grant proposals at S&P/ASX300 AGMS during 2025. This Deep Dive article takes our analysis further, exploring some interesting correlations and trends underpinning the headline remuneration voting data.

Correlation between remuneration strikes and significant votes against equity grant awards

Interestingly, of the 33 companies across the S&P/ASX300 that received a strike in 2025, nearly half (16 issuers, or 48.5%) also faced significant opposition (10% or more votes against) to their forward-looking equity grant proposals. On average since 2019, 46.1% of issuers that received a strike also received at least 10% of votes against their equity grants.

This consistent pattern shows that many investors that are unhappy with the company’s current or past remuneration practices on an ‘advisory’ voting basis will often back that up with opposition to the incentive pay arrangements being proposed for future rewards to executives as well.

- In this sub-group, it would appear that investors have ongoing concerns about structural flaws or misalignments inherent in companies’ remuneration approach, which are likely to persist in votes against remuneration reports in future years unless rectified.

On the other hand, the other 17 companies in this cohort that received strikes in 2025 (51.5%) - and a broadly similar proportion in previous years - did not see investor dissent against remuneration reports extending to significant pushback against forward-looking pay grants.

- In these cases it appears that investors’ objections to the remuneration report were driven more by concerns over past remuneration practices not future ones - or sometimes by investor concerns that were not necessarily related to remuneration at all; i.e. the remuneration report votes were more a general protest vote designed to send a message to companies about broader governance or culture and conduct issues.

The different scenarios reflected in these results should help guide issuers that have experienced a remuneration strike in interpreting the underlying causes and considering actions that should be taken in 2026.

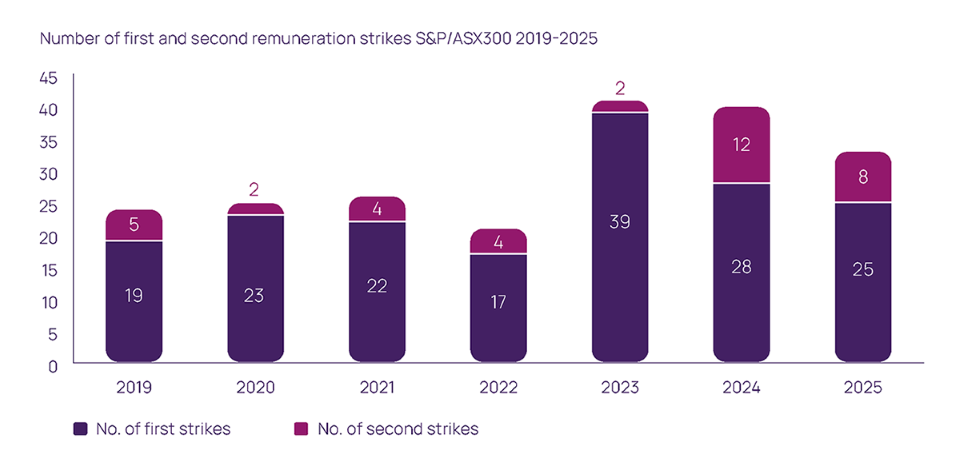

Second strikes – practical implications

Of the 33 strikes experienced across the S&P/ASX300 in 2025, eight were second strikes.

Although this number is lower than the equivalent in 2024 (12), it remains high compared to all years between 2019 and 2023, suggesting a persistence of shareholder concerns related to unresolved remuneration issues.

Among the eight issuers receiving a second strike in 2025, seven1 board spill resolutions were put forward at AGMs (Australian Clinical Labs, ANZ Group Holdings, CSL, IDP Education, NRW Holdings, Reece and Reliance Worldwide Corporation). Investors overwhelmingly rejected these board spill proposals, with average support of just 4.5%. ‘Against’ votes ranged from 86.6% (Australian Clinical Labs) to 98.6% (ANZ Group Holdings).

So, despite the continued significant incidence of strikes, experience in 2025, as in prior years, shows that most institutional investors routinely avoid destabilising boards by not supporting the ultimate sanction of ‘spilling’ the board, even in cases where they have expressed continued opposition to a company’s remuneration report for two or more successive years.

Serial strike recipients

In one corner of the market, there is a small number of S&P/ASX300 issuers who have become ‘serial’ strike recipients; i.e. they routinely incur remuneration strikes each and every year. In fact, of the 33 strikes, a total of 13 companies recorded two or more consecutive strikes.

A common characteristic among these issues is that they generally have more concentrated share registers with a higher proportion of insider or management-friendly shareholders. This means that they are much less likely to ever be exposed to a board spill in practice, as they generally have the numbers to ensure continuity of incumbent directors and management.

| Technical strike in 2025 | Actual strikes in a row | |

| Brainchip Holdings | First strike | Third strike |

| Champion Iron | First strike | Third strike |

| Clinuvel Pharmaceuticals | First strike | Third strike |

| Dicker Data | First strike | Fifth strike |

| Lovisa Holdings | First strike | Fifth strike |

| NRW Holdings | Second strike | Eighth strike |

It would appear that these companies have in effect made a calculated risk assessment that they can withstand any implicit threat of investor dissent or board spills from non-associated investors, even over periods that exceed the 2-yearly ‘strike’ cycle.2

Reputation risk

These outcomes confirm that, from a technical legal perspective, the spill provision is largely “symbolic”, especially in the larger-capitalisation segment of the Australian market where an individual strategic investor is less likely to have the numbers to force a ‘spill’ through their own holdings alone.

Yet whatever the formal legal implications, there is no doubt that for high-profile and ‘brand name’ companies in particular, remuneration strikes invariably attract intense public and media scrutiny, and can present significant reputation management challenges to boards and executives of ASX listed companies.

This was very much the lived experience of some prominent blue-chip companies at the top end of the S&P/ASX300 – notably CSL, Macquarie Group and ANZ Group Holdings, all of which received remuneration strikes during 2025 amid highly-publicised controversies around strategic, regulatory and/or financial performance issues.

As we noted in last year’s AGM Review, in this context the remuneration vote has become in effect an annual referendum on overall investor sentiment around ASX companies, and a key barometer of corporate reputation and stakeholder alignment in the eyes of key external stakeholders.

In November 2025 the Australian Securities and Investments Commission (ASIC) issued a report3 highlighting how the two-strikes rule has grown its influence and complexity since it was introduced in 2011. ASIC’s report noted that, whilst originally intended as a mechanism to give shareholders a meaningful voice on executive pay, the rule is increasingly used as a broader protest tool.

ASIC acknowledged concerns in this regard from directors and issuers, noting that the rule’s application in a wider context is a complex policy issue for the government to consider. While strike numbers have surged in recent years, the Australian regime remains unique globally and continues to shape governance practices.

The voting outcomes and historical outcomes detailed above reinforce this point of view.

For S&P/ASX300 companies, the takeaway is clear: while the practical risk of a successful spill is minimal, reputational and engagement risks tied to strikes are significant and demand proactive management.

1 The exception was James Hardie Industries which as a foreign-domiciled issuer is not subject to the formal legal impacts of the Australian two-strikes rule. So, they were not required to submit a board spill resolution to their AGM despite incurring a vote of over 25% ‘against’ their remuneration report for two successive AGMs.

2 Technically, the ‘two strikes’ rule re-sets to zero after a second strike is incurred (i.e. a third successive strike counts as a first strike in terms of its legal effect). Our definition of a serial strike recipient is for those companies receiving three or more consecutive strikes.

3 Advancing Australia's evolving capital markets: Discussion paper response report